Managing infertility can be stressful, isolating and financially burdensome for patients. Their physicians have the difficult task of guiding them emotionally and logistically through the myriad of available treatment options. Assisted reproductive technology (ART) is expensive, especially in the United States, and IVF insurance coverage is inconsistent.

Health insurance carriers in 15 states are mandated to cover in vitro fertilization, according to The National Infertility Association; in an additional two states, insurance companies are required to merely offer coverage. There are some notable exceptions to coverage, however. For example, in some states, legislation allows age cut-offs, requires that prospective parents be married and allows religious exemptions for certain employers. Reproductive specialists should stay up to date on the insurance and financial options available to their patients, as well as international developments in IVF funding that could one day arrive on their doorstep.

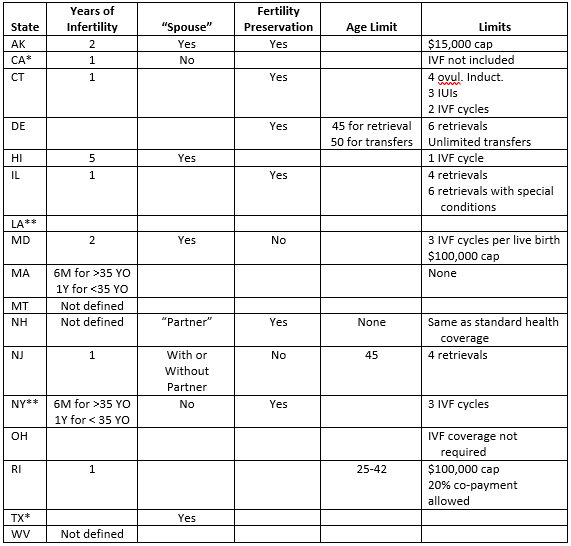

Coverage in States Where Services Are Mandated By Law

Even in states where coverage is legally mandated, coverage varies greatly. Some states clearly define who is covered, and for what services, while other states do not offer guidance. California — one of two states that only requires offering coverage — appears to be the only state that restricts discriminating against patients seeking IVF services on the basis of factors like age, gender or sexual orientation. However, other states include language extending coverage to unmarried, gender-neutral "partners" or even insured individuals without partners.

The table below offers specific information for states that are required to cover treatment, and for those required to offer coverage. Note that some small businesses or employers who self-insure are exempt from these requirements in many of these states. Cells that are empty are not addressed in the state regulations.

Table of IVF Coverage By State

*Required to offer.

**NY prohibits the exclusion of coverage, but does not mandate coverage.

If you treat patients in a state where IVF is covered, it is important to seek preauthorization before starting any treatments. Patients may need counseling on the types of questions they should ask their insurance company to understand which tests and medications are covered under their plans.

Medically necessary testing and imaging — such as an ultrasound to assess the potential causes of infertility — is typically covered, but this is just a small piece of the process. Even if a patient's coverage includes IVF, their individual plans may not allow it until they've attempted intrauterine insemination a specified number of times. Plans may cover pre-implantation genetic testing if it is deemed "medically necessary," but that is a distinction defined under the insurer's terms. Additionally, if the insurance company is not based in the state where coverage is mandated, it may not provide IVF insurance in the state where an individual patient resides.

How the U.S.A Compares Worldwide

The Centers for Disease Control and Prevention (CDC) states that less than 2 percent of live births in the U.S.A. result from IVF. The cost of IVF is highest in the U.S.A., although there is a small trend toward lower-cost services. Japan has the highest rate of birth from IVF — 5 percent — but also success rates of only about 20 percent. According to Eurobiz Japan, the country's national health system does not cover the costs of IVF. However, women under the age of 43 who meet income requirements are eligible for subsidies that cover the cost of the first IVF cycle (about $4,500 at the March 2020 exchange rate) and provide partial coverage for subsequent cycles. Many infertility clinics in Hawaii market their location as an IVF destination for Japanese women, since U.S.A. success rates are much higher, preimplantation genetic testing is offered and the clinics are relatively close in distance to Japan. Since 1 in 5 or 6 Japanese couples struggle with infertility and the birth rate is at its lowest since 1899, according to The Japan Times, concerns about population decline have prompted the government to implement policies encouraging child rearing.

For European patients, IVF insurance coverage varies across countries and regions. According to the European Society for Human Reproduction and Embryology (ESHRE), Ireland, Cyprus and Lithuania are the only European Union states that do not provide state-funded, publicly accessible IVF.

Funding is variable among countries that do cover IVF; Germany funds around 50 percent of treatment costs, according to ESHRE, while Belgium and France cover the complete costs of four to six treatment cycles for eligible patients. ESHRE notes that the lowest level of funding is in Bulgaria, Romania and Spain (20-30 percent), while Greece, the Netherlands and Slovenia provide around 90 percent funding.

Changing Success Rates and the Need for Advocacy

Research published in Human Reproduction Open reports that success rates per fresh cycle of IVF, regardless of maternal age, peaked in 2010 at about 30 percent and have now fallen to roughly 25 percent, or the same as in 1998. The review examined a number of studies that attempted to account for this decline in success rates by considering newer techniques and tests that may have hampered progress. For example, preimplantation genetic testing and "closed embryo incubation with time lapse imaging" have been criticized for high numbers of false-positive tests, which reduce the number of embryos that would result in live births. Mild ovarian stimulation, meanwhile, may lower success rates by reducing the number of available embryos.

On an individual level, however, patients in the United States may face the greatest cost-related challenges to overcoming infertility. The Fertility IQ Family Builder Workplace Index found that in 2018, 71 percent of women surveyed who received IVF services did so with no IVF insurance coverage. However, the index also reports an uptick in the number of companies that added or improved existing fertility insurance coverage between 2017 and 2018.

Advocacy groups urge individuals to ask their employers to add policies that cover IVF. A good impetus for employers to offer IVF insurance is that individuals paying for IVF themselves are more likely to transfer multiple embryos, leading to a higher rate of multiple births, according to research from Fertility and Sterility. Multiple births are far more costly than singleton births in terms of both financial burden and risks to maternal and fetal health.

Many reproductive specialists experience the joy of helping individuals achieve healthy pregnancies, but this process presents unique mental and financial challenges. Physicians can help relieve some of this burden by staying aware of the prohibitive costs, ensuring that the patient's insurance is billed for all allowable costs and encouraging patients to advocate for better coverage from their employers and legislators.